SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2013

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE EXCHANGE ACT

Commission file number: 000-53704

AMP HOLDING INC.

(Name of registrant as specified in its charter)

|

Nevada

|

26-1394771

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

100 Commerce Drive

|

|

|

Loveland, Ohio 45140

|

513-360-4704

|

|

(Address of principal executive offices)

|

(Registrant’s telephone number)

|

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE EXCHANGE ACT:

None

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE EXCHANGE ACT:

Common Stock, $0.001 par value per share

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 of Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer o

|

Smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of June 29, 2012, the last business day of the Registrant’s most recently completed second fiscal quarter, the market value of our common stock held by non-affiliates was $5,499,297.

The number of shares of the Registrant’s common stock, $0.001 par value per share, outstanding as of April 15, 2014, was 76,622,130.

|

PART I

|

||

|

4

|

||

|

9

|

||

|

13

|

||

|

14

|

||

|

14

|

||

|

14

|

||

|

PART II

|

||

|

14

|

||

|

22

|

||

|

22

|

||

|

25

|

||

|

F-1

|

||

|

26

|

||

|

26

|

||

|

27

|

||

|

PART III

|

||

|

27

|

||

|

29

|

||

|

33

|

||

|

33

|

||

|

34

|

||

|

PART IV

|

||

|

35

|

||

|

38

|

Forward-Looking Statements

The discussions in this Annual Report contain forward-looking statements reflecting our current expectations that involve risks and uncertainties. When used in this Report, the words “anticipate”, expect”, “plan”, “believe”, “seek”, “estimate” and similar expressions are intended to identify forward-looking statements. These are statements that relate to future periods and include, but are not limited to, statements about the features, benefits and performance of our products, our ability to introduce new product offerings and increase revenue from existing products, expected expenses including those related to selling and marketing, product development and general and administrative, our beliefs regarding the health and growth of the market for our products, anticipated increase in our customer base, expansion of our products functionalities, expected revenue levels and sources of revenue, expected impact, if any, of legal proceedings, the adequacy of liquidity and capital resource, and expected growth in business. Forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those projected. These risks and uncertainties include, but are not limited to, market acceptance for our products, our ability to attract and retain customers for existing and new products, our ability to control our expenses, our ability to recruit and retain employees, legislation and government regulation, shifts in technology, global and local business conditions, our ability to effectively maintain and update our product and service portfolio, the strength of competitive offerings, the prices being charged by those competitors and the risks discussed elsewhere herein. These forward-looking statements speak only as of the date hereof. We expressly disclaim any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

All references in this Form 10-K that refer to the “Company”, “AMP Holding", "AMP", “we,” “us” or “our” are to AMP Holding Inc. and unless otherwise differentiated, its wholly-owned subsidiary, AMP Electric Vehicles Inc.

PART I

We design, develop, manufacture, and sell high-performance, medium-duty trucks with advanced powertrain components under the Workhorse proven chassis brand. We believe that our vehicles, engineering expertise, innovation, and operational structure differentiate us from traditional truck manufacturers.

We recently announced that we filed a provisional patent for a new system that extends the range of electric vehicles while reducing the overall cost of the typical battery-electric power train. The new system, E-GEN Drive(TM), is designed specifically for the package delivery vehicle market, in which the diesel and/or gasoline-powered vehicles in use now, stop and restart hundreds of times a day. We believe that battery-electric technology is an ideal fit for urban and suburban delivery routes and we understand fleet owner's concerns about range anxiety and cost. Our E-GEN Drive system will enable them to keep the batteries recharged to a consistent state of charge throughout the day and, since we are able to use smaller battery packs, we can reduce the cost of the entire system. Our E-GEN Drive trucks, offer a three-year payback making them price competitive with gasoline-powered trucks.

Our association with Power Solutions International (PSIX:NASDAQ) provides us with multi-fuel engines that function as generators. When the ignition is shut off, the engine automatically turns on and recharges the battery pack. When the ignition is turned back on, the engine turns off and the vehicle reverts to all-electric power. The engine and the battery-powered motor are never in use at the same time. It's not a traditional hybrid, but an extended-range electric vehicle.

As a result, we believe our new design has many benefits, including:

|

·

|

Fleet management flexibility: Depending on our customer’s driving patterns and fuel cost goals, our E-GEN drive train can be remotely adjusted to use more electric power or internal combustion engine (ICE) power at their choice.

|

|

·

|

Energy efficiency and cost of ownership: We believe our trucks offer our customers an attractive cost of ownership profile when compared to similar products. Using a single electric powertrain with a small ICE enables us to create a lighter, more energy efficient vehicle that is mechanically simple. Since we are able to use smaller battery packs, we can reduce the cost of the entire system. Additionally, government incentives can reduce the cost of ownership even further.

|

|

·

|

High performance: We believe our trucks deliver an unparalleled driving experience with powerful acceleration for the most demanding applications with the added benefit of a very quiet operation.

|

We also announced the second generation, full-electric truck “E-100” which is a significant improvement to our first generation vehicle. The second-generation vehicle includes a single powerful electric motor with no transmission and new lighter, high-density Lithium Ion batteries giving the vehicle a range of up to 100 miles.

In March of 2013, we purchased the former Workhorse Custom Chassis assembly plant in Union City, Indiana from Navistar International (NAV:NYSE). This assembly plant has consistently produced more than $100 million dollars of revenue per year since 2003. With this acquisition, we became an Original Equipment Manufacturer (OEM) of Class 3-6 commercial-grade, medium-duty truck chassis to be marketed under the Workhorse® brand.

Ownership and operation of this plant enables us to build new chassis with gross vehicle weight capacities of between 10,000 and 26,000 pounds and offer them in four different fuel variants—electric, gas, propane, and compressed natural gas (CNG). We plan to offer commonly known Workhorse chassis like the W22, W42, W62, as well as a new, 88” track, W88 truck chassis that will be offered to fleet purchasing managers at price points that are both attractive and cost competitive.

At the same time, AMP intends to partner with engine suppliers and body fabricators to offer fleet-specific, custom, purpose-built chassis that provide total cost of ownership solutions that are superior to the competition.

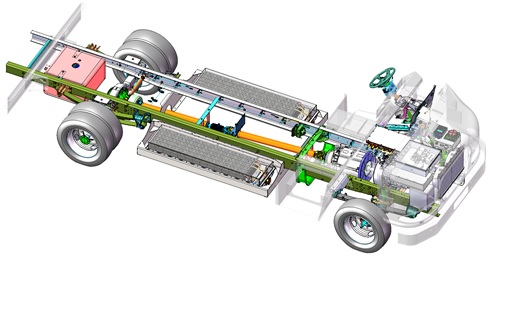

In addition to having the ability to build our own chassis, we design and produce battery-electric power trains that can be installed in new Workhorse chassis or installed as repower packages to convert used Class 3-6 medium-duty vehicles from diesel or gasoline power to electric power. Our approach is to provide battery-electric power trains utilizing proven, automotive-grade, mass-produced parts in its architecture coupled with in-house control software that we have developed over the last five years.

The Workhorse Custom Chassis acquisition includes other important assets including the Workhorse brand and logo, intellectual property, schematics, logistical support from Up-Time Parts (a Navistar subsidiary) and, perhaps most importantly, a network of 400-plus sales and service outlets across North America. We believe combination of AMP’s chassis assembly capability, coupled with its ability to offer an array of fuel choices, gives AMP/Workhorse a unique opportunity in the marketplace.

Our Products

Powertrain:

E-GEN

In January of 2014, AMP Holdings Inc. submitted a patent application for a new drive system. This revolutionary design is an extended range electric drive system that we call the E-GEN. This system is an electric drive that has a gasoline/propane or CNG engine that functions as an auxiliary generator that only runs when the battery reaches a certain level of depletion, the vehicle is in PARK and the key is out. This system combines battery-electric propulsion with a low-horsepower, fossil fuel generator to produce a vehicle that gets two to four times the miles per gallon of its conventional counterpart, thus providing the fleet operator with a solution that has a three-year payback without any government incentives. We believe that this is the ideal solution for the domestic package delivery fleet operators as well as other specialized markets (i.e. shuttle, school, public transportation buses, and specialty-use vehicles). We are currently working with the California Air Resource Board (CARB) and the Environmental Protection Agency (EPA) to get approval for this design so it can qualify for governmental incentives.

Our approach to the commercial market is to provide alternative-fueled chassis at competitive prices that are as reliable and consistent, in all aspects, as the Navistar chassis that last rolled off the line in the last quarter of 2012. Our sales strategy targets the Top Fleet Buyers. We have restored purchasing arrangements with key parts suppliers, forged an arrangement for logistics support with UpTime Parts, Inc. and structured an engine supply agreement with Power Solutions International (NASDAQ:PSIX).

We are focused on the extended range electric E-GEN solution since it offers the customer a solution that provides answers to their key concerns with electric vehicles (i.e. range issues in cold weather, peak season requirements, infrastructure costs, and “what are my options if there is a power outage?”).

E-100

Our AMP E-100 all-electric, medium-duty truck is the second generation full electric power-train that is a significant improvement to our first generation. It includes a single electric motor with no transmission and new lighter, high-density Lithium Ion batteries giving it a range of up to 100 miles. This application has received California Air Resources Board approval for sale in California and is now on the California HVIP list and eligible for incentive purchase. Additionally, we are also approved in New York under the NYSERDA Program and approved for both new trucks and repowers under the Drive Clean Chicago incentive program.

Chassis:

W88

The new W88 chassis is designed to meet the needs of a wide range of customers. At the same time, it is a universal chassis from an operations perspective. We believe that this chassis will be the workhorse of our product offerings. We expect to offer this chassis with gross vehicle weight GVW ratings of 10,000 to 26,000 pounds. It will also be offered with drive train and fuel systems ranging from all-electric , extended range electric EREV utilizing gasoline, propane or CNG, PSI gasoline 6-liter engine, propane, and CNG.

W22

The W22 chassis is designed to meet the needs of the recreational vehicle market for weight ratings up to 26,000 GVW. It has been in the marketplace for over 10 years and is well-proven for this application. We will offer this chassis with the PSI 8.8 Liter engine.

W42

The W42 chassis is designed for the 12,000 to 14,500 GVW vehicle market. Like the W22 it has been in the marketplace for over 10 years and is well-regarded.

W62

The W42 chassis is designed for the 19,500 to 23,500 GVW vehicle market. Like the W22 and W42 it has been in the marketplace for over 10 years and is also well-proven.

Applications for these Products:

Commercial Step Vans

Package Delivery Industry: Approximately 80% of the vehicles in this segment operate on a fixed route and travel fewer than 100 miles per day, stop more than 100 times within an average duty cycle of eight to ten hours, and return to an indoor distribution center. The best examples include: UPS, FEDEX, FEDEX Ground, DHL, and Purolator.

Product Delivery Industry: Approximately 70% of the vehicles in this segment operate on a fixed route and travel fewer than 100 miles per day, stop between 50 and 100 times within an average duty cycle of eight to ten hours, and return to a distribution center that is either indoors, or the vehicles are stored at the dock, or in an outdoor lot adjacent to the distribution facility. Examples are: Frito-Lay, Pepsi, Coke, Aramark, Bimbo Bakeries, Peapod, and other grocery delivery services.

Laundry and Uniform Service Industry: Approximately 60% of the vehicles in this segment operate on a fixed route and travel approximately 100 miles per day, stop between 30 and 50 times within an average duty cycle of eight to ten hours, and return to a laundry facility where the vehicles are stored outside the facility. Cintas, Aramark, UniFirst, and Diaper Service are examples.

Food Service Industry: Approximately 80% of the vehicles in this segment operate on a fixed route and travel approximately 100 miles per day stopping between 10 and 30 times within an average duty cycle of eight to ten hours. They return to a commissary facility where the vehicles are stored outside the facility and serviced at this common facility. Food trucks fall into this category.

Utility Industry: The route that these vehicles follow is dependent on the utility and the energy company’s territory. Some utilities, for example, are captive to a county or surrounding counties of one large metro area. This model is ideal for a segment of the fleet to be all electric utility vehicles. For the utilities that cover the entire state or even multiple states, CNG, or Hybrid CNG/Electric vehicles are required.

Special Use Industry: This segment basically consists of what is not already mentioned. SWAT, Warehouse on Wheels i.e. Snap-on-Tools, HVAC, Plumbers, and other service applications that require a large cube storage vehicle fit into this category.

The current number of commercial step vans in use in the US is approximately 300,000 units. Today between 3% and 4% are replaced with new vehicles every year. A number of the larger fleets that effectively utilize this type of vehicle replace vehicles at a rate closer to 7% per year. We believe that with the proper mix of alternative fuel options combined with purpose-built chassis for specific use in this segment will result in a replacement rate of as much as 10% in the initial transition period and then a 5% to 7% overall rate long term.

Medium Duty Buses

The next segment that we believe will have significant volume potential for us is the medium duty bus (108”H x 95.5 W x 247”to 286” L) Para-Transit, Shuttle and School Buses are part of this segment. We are able to offer alternative fuel solutions, as well as innovative E-GEN EREV solutions combined with the AMP/Workhorse chassis.

Special Use Vehicles

The special use vehicle segment includes emergency vehicles, wreckers, construction equipment, communications equipment and military base application. This segment is similar to Medium-duty buses in terms of volume potential.

Recreational Vehicles

In 2006, the Union City, IN Workhorse facility produced close to 20,000 RV chassis. The high-volume point for this total segment was 70,000 new units per year at which time Workhorse produced approximately 30% of that volume. RV Sales in 2012 were approximately 25,000 and sales are projected to grow in the next few years. Our ability to offer a gasoline, propane, or CNG RV would allow us to offer an additional unique product in this segment.

Technology

Batteries Are Key

The battery pack is key to the design, development, and manufacture of advanced electric-vehicle power trains. Where some other EV manufacturers purchase their batteries in a plug-and-play pack, we build our own battery packs. This keeps the intellectual property related to the design and production of the pack in-house and avoids the issues that occur when a battery supplier fails. And it also enables us to pay less for our batteries and pack than do our competitors thus our all-electric truck is less expensive than competitive vehicles. We use the Panasonic or LG Chem 18650 cells and, like Tesla, design the pack around these commodity cells.

In-House Software Development is Essential

Our power trains encompass the complete motor assemblies, computers, and software required for vehicle electrification. We use off-the-shelf, proven components and combine them with our proprietary software.

Innovation is the Future

Additionally, we have developed a cloud-based, remote management system to manage and track the performance of all of the vehicles that we deploy in order to provide a 21st Century solution for fleet managers.

Locations and Facilities

Our company headquarters and R & D facility is located at 100 Commerce Drive, Loveland, Ohio, a Cincinnati suburb. We occupy a 30,000 sq. ft. facility that allows for the manufacture of 1,000 electric power train kits per year. Power trains will be delivered to the Workhorse facility in Indiana or shipped to our dealer network for onsite installation in conversion vehicles.

Workhorse/AMP Trucks, Inc. Location

Our truck assembly facility is located in Union City, Indiana. This facility consists of three buildings with 270,000 square feet of manufacturing and office space on 46 acres.

|

Workhorse Facility

In March of 2013, we purchased the former Workhorse Custom Chassis assembly plant in Union City, Indiana. This assembly plant has consistently produced more than $100 million dollars of revenue per year since 2003. With this acquisition, we became an Original Equipment Manufacturer (OEM) of Class 3-6 commercial-grade, medium-duty truck chassis to be marketed under the Workhorse® brand.

Ownership and operation of this plant enables us to build new chassis with gross vehicle weight capacity of between 10,000 and 26,000 pounds and offer them in four different fuel variants—electric, gas, propane, and CNG. We plan to offer well- known Workhorse chassis like the W22, W42, W62, as well as a new, 88” track W88 truck chassis that will be offered to fleet purchasing managers at price points that are both attractive and cost competitive.

|

|

At the same time, AMP intends to partner with engine suppliers and body fabricators to offer fleet-specific, custom, purpose-built chassis that provide total cost of ownership solutions that are superior to the competition.

In addition to building our own chassis, we design and produce battery-electric power trains that can be installed in new Workhorse chassis or installed as repower packages to convert used Class 3-6 medium-duty vehicles from diesel or gasoline power to electric power. Our approach is to provide battery-electric power trains utilizes proven, automotive-grade, mass-produced parts in its architecture coupled with in-house control software that it has developed over the last five years.

The Workhorse Custom Chassis acquisition includes other important assets including the Workhorse brand and logo, intellectual property, schematics, logistical support from UpTime Parts (a Navistar subsidiary) and, perhaps most importantly, a network of 400 plus sales and service outlets across North America. We believe the combination of AMP’s chassis assembly capability, coupled with its ability to offer an array of fuel choices, gives AMP/Workhorse a unique opportunity in the marketplace.

Marketing

Our sales team is focused on a targeted list of high profile, former purchasers, and current buyers of the Workhorse chassis with the goal of securing purchase orders from these companies. These purchase orders will give us the first look at next year’s chassis demand related to electric and extended range electric vehicles.

Our priority is to establish the commercial step van as our core business. We intend to be the best choice for a vehicle in this segment regardless of the fuel type that the customer chooses. Additionally, our sales plan is to meet with the top potential customers and obtain purchase orders for new electric, extended range electric, gasoline, propane, or CNG vehicles for their production vehicle requirements.

The second segment that we are focused on is medium-duty buses. This is based on fact that we completed two 15-passenger para-transit buses for BARTA (Berks County Regional Transit Authority) in Pennsylvania. These buses are equipped with wireless charging and represent a unique solution for a number of applications (i.e. airport hotels, rental car companies and municipal transit authorities). Once we have completed all of the relevant testing on these buses we will work with bus body builders to develop pricing and plan to offer a Workhorse/AMP chassis for sales in late 2016.

Finally, since our competitive advantage in the marketplace is our ability to provide purpose-built solutions to customers that have unique requirements at relatively low-volume, we have submitted proposals to companies for purpose-built vehicle applications.

AMP Trucks will promote the Workhorse brand at select trade shows, conferences and briefings. In 2013, AMP exhibited at ACT 2013 (the Alternative Clean Transportation) Expo in Washington, DC, and Steve Burns, AMP CEO, was a speaker at the event. We also exhibited at High Efficiency Truck User Forum in Chicago in 2013 and demonstrated an AMP E-100 in the Ride and Drive. With the completion of demonstration vehicles, we will be able to have vehicles on site at Ride and Drives events and/or static display vehicles for our trade show activities that include the ACT 2014 show in Long Beach, CA in May 2014.

Strategic Relationships

Power Solutions International (PSIX:NASDAQ): PSI supplies engines that are certified and calibrated for on-road use by companies such as AMP/Workhorse utilizing gasoline, propane or CNG as a fuel. They have the ability and the resources to provide engines that meet fleet requirements in volumes that are significantly below the volume requirements of companies like Ford or Freightliner for similar specialized powertrain systems.

Morgan Olsen, Utilimaster, TransTech Bus, ECO, and other up-fitters or body fabricators: All of these companies build bodies customized for the needs of their customers and mated to chassis that are available to them from the short list of chassis suppliers. The functionality and configuration the end-user receives in the finished product is limited by the available chassis/powertrain. AMP/Workhorse will work with these organizations to provide chassis that not only best fit the needs of the end user customer but also provide the customer with a competitive advantage in their specific industry or application.

Research and Development

The majority of our research and development is conducted in-house at our facilities near Cincinnati, Ohio. Additionally, we contract with engineering firms to assist with validation and certification requirements as well as specific vehicle integration tasks.

Competitive Companies

There are two primary competitors in the medium-duty vehicle segment in the US market: Ford and Freightliner. Neither has disclosed any plans to offer 100% EV or EREV vehicles in this segment. Ford is vertically integrated building a complete vehicle or chassis including Ford engine & transmission. They provide a chassis as a strip-chassis (which is similar to the Workhorse product) or they provide it with a cab. Ford vehicles tend to be of a lighter design than that of either Workhorse or Freightliner. For this segment Freightliner provides a chassis as a strip-chassis, which is similar to the Workhorse/AMP Truck chassis.

We believe the most dramatic difference between AMP and the other competitors in the medium duty truck market is our ability to offer customers purpose-built solutions that meet the needs of their unique requirements at a competitive price. While there are many electric car companies from abroad, there are only a few foreign companies that have vehicles in the category of medium-duty trucks.

Intellectual Property

The company has multiple pending U.S. patent applications and also plans to pursue appropriate foreign patent protection on those inventions. The company also has five pending trademark applications and two issued trademark registrations in the U.S. with intent to pursue foreign trademark registration as well.

Agreements

Momentum Dynamics and BARTA (Berks County Regional Transportation Authority)

On December 29, 2012, the Company entered into an Agreement with Momentum Dynamics to engineer, develop, and produce two development vehicles for BARTA in Reading, Pennsylvania. We are seeking to have this project generate the following: promote the use of AMP products for other similar applications i.e. rental car shuttle buses, motel and hotel shuttle buses, school buses, and other hospitality shuttle bus applications, network the AMP products through the Momentum Dynamic sales channel, and promote the sale of AMP products to the Departments of Transportation throughout the US.

Navistar International Truck

In April of 2012 we signed a development agreement with Navistar International Truck. The scope of work for this project was to repower two 2004 vintage W1652 vehicles, which were originally produced by Navistar. Their customer, a large package delivery company, has an interest in repowering these vehicles with something other than the current diesel engine that is in this vehicle. Navistar was interested in working with them to repower these vehicles with either electric or some other fuel system. With electric being the most desirable if the customer’s price point could be met, AMP was subcontracted by Navistar to perform the electric repower, and in August of 2012 AMP delivered the first vehicle to Navistar. The vehicle passed their initial performance requirements which were based on their end customer’s specifications. In October 2012 Navistar turned the project over to AMP to work directly with them to provide a 100% electric repowered vehicle. Since that time, AMP has been working through the customer requirements and is in the final stages of testing and durability. Once all testing is completed we plan on finalizing purchase orders that are currently in the discussion phase.

We require capital for our operations as we are currently significantly undercapitalized and if we are unable to raise capital in the near future we will cease operations.

Our cash balance as of the end of March 2014 was $2.7M. This may impact the payment of our outstanding accounts payable balance. We are currently evaluating several options for financing, but there are no guarantees that we will raise capital or that if we do raise the capital it will be on acceptable terms.

Our limited operating history makes it difficult for us to evaluate our future business prospects and make decisions based on those estimates of our future performance.

We have basically been a research and development company since beginning operations in February 2007. We have a limited operating history and have generated limited revenue. As we move more toward a manufacturing environment it is difficult, if not impossible, to forecast our future results based upon our historical data. Because of the uncertainties related to our lack of historical operations, we may be hindered in our ability to anticipate and timely adapt to increases or decreases in revenues or expenses. If we make poor budgetary decisions as a result of unreliable historical data, we could be less profitable or incur losses, which may result in a decline in our stock price.

Failure to successfully integrate the Workhorse ® brand, logo, intellectual property, patents and assembly plant in Union City, Indiana into our operations could adversely affect our business and results of operations.

As part of our strategy to become an OEM, in March 2013, we have acquired Workhorse and the Workhorse Assets including the Workhorse ® brand, logo, intellectual property, patents and assembly plant in Union City, Indiana. The Workhorse acquisition may expose us to operational challenges and risks, including the diversion of management’s attention from our existing business, the failure to retain key Workhorse dealers and our ability to commence operations at the plant in Union City, Indiana. Our ability to sustain our growth and maintain our competitive position may be affected by our ability to successfully integrate the Workhorse Assets.

AMP’s results of operations have not resulted in profitability and we may not be able to achieve profitability going forward.

AMP has incurred net losses amounting to $27,481,812 for the period from inception (February 20, 2007) through December 31, 2013. In addition, as of December 31, 2013, AMP has a working capital deficiency of $ 4,020,840. If we incur additional significant operating losses, our stock price may decline, perhaps significantly.

Our management is developing plans to alleviate the negative trends and conditions described above. Our business plan has changed from concentrating on EV SUV’s to EV medium duty trucks, but is still speculative and unproven. There is no assurance that even if we successfully implement our business plan, that we will be able to curtail our losses. Further, as we are a development stage enterprise, we expect that net losses and the working capital deficiency will continue.

Our business, prospects, financial condition and operating results will be adversely affected if we cannot reduce and adequately control the costs and expenses associated with operating our business, including our material and production costs.

We incur significant costs and expenses related to procuring the materials, components and services required to develop and produce our electric vehicles. As a result, our current cost projections are considerably higher than the projected revenue stream that such vehicles will produce. As a result we are continually working on initiatives to reduce our cost structure so that we may effectively compete.

We currently do not have long-term supply contracts with guaranteed pricing which exposes us to fluctuations in component, materials and equipment prices. Substantial increases in these prices would increase our operating costs and could adversely affect our business, prospects, financial condition and operating results.

Because we currently do not have long-term supply contracts with guaranteed pricing, we are subject to fluctuations in the prices of the raw materials, parts and components and equipment we use in the production of our vehicles. Substantial increases in the prices for such raw materials, components and equipment would increase our operating costs and could reduce our margins if we cannot recoup the increased costs through increased vehicle prices. Any attempts to increase the announced or expected prices of our vehicles in response to increased costs could be viewed negatively by our customers and could adversely affect our business, prospects, financial condition and operating results.

We depend upon key personnel and need additional personnel.

Our success depends on the continuing services of James E. Taylor, Chairman of the Board, Stephen Burns, CEO, and Martin J. Rucidlo, President. The loss of any of these individuals could have a material and adverse effect on our business operations. Additionally, the success of the Company’s operations will largely depend upon its ability to successfully attract and maintain competent and qualified key management personnel. As with any company with limited resources, there can be no guarantee that the Company will be able to attract such individuals or that the presence of such individuals will necessarily translate into profitability for the Company. Our inability to attract and retain key personnel may materially and adversely affect our business operations.

We must effectively manage the growth of our operations or our company will suffer.

To manage our growth, we believe we must continue to implement and improve our operational, manufacturing, and research and development departments. We may not have adequately evaluated the costs and risks associated with this expansion, and our systems, procedures, and controls may not be adequate to support our operations. In addition, our management may not be able to achieve the rapid execution necessary to successfully offer our products and services and implement our business plan on a profitable basis. The success of our future operating activities will also depend upon our ability to expand our support system to meet the demands of our growing business. Any failure by our management to effectively anticipate, implement, and manage the changes required to sustain our growth would have a material adverse effect on our business, financial condition, and results of operations.

Our business requires substantial capital, and if we are unable to maintain adequate financing sources our profitability and financial condition will suffer and jeopardize our ability to continue operations.

We require substantial capital to support our operations. If we are unable to maintain adequate financing, or other sources of capital are not available, we could be forced to suspend, curtail or reduce our operations, which could harm our revenues, ability to achieve profitability, financial condition and business prospects.

We face competition. A few of our competitors have greater financial or other resources, longer operating histories and greater name recognition than we do and one or more of these competitors could use their greater resources and/or name recognition to gain market share at our expense or could make it very difficult for us to establish market share.

In the electric medium duty truck market in the United States, we compete with a few other manufacturers, including EVI and Smith Electric, who have more significant financial resources, established market positions, long-standing relationships with customers and dealers, and who have more significant name recognition, technical, marketing, sales, financial and other resources than we do. Each of these companies is currently selling an electric vehicle or is working to develop, market and sell advanced technology vehicles in the United States market. The resources available to our competitors to develop new products and introduce them into the marketplace exceed the resources currently available to us. As a result, our competitors may be able to compete more aggressively and sustain that competition over a longer period of time that we can. This intense competitive environment may require us to make changes in our products, pricing, licensing, services, distribution, or marketing to develop a market position. Each of these competitors has the potential to capture market share in our target markets which could have an adverse effect on our position in our industry and on our business and operating results.

If we are unable to keep up with advances in electric vehicle technology, we may suffer a decline in our competitive position.

There are companies in the electric vehicle industry that have developed or are developing vehicles and technologies that compete or will compete with our vehicles. We cannot assure that our competitors will not be able to duplicate our technology or provide products and services similar to ours more efficiently. If for any reason we are unable to keep pace with changes in electric vehicle technology, particularly battery technology, our competitive position may be adversely affected. We plan to upgrade or adapt our vehicles and introduce new models in order to continue to provide electric vehicles that incorporate the latest technology. However, there is no assurance that our research and development efforts will keep pace with those of our competitors.

Our electric vehicles compete for market share with vehicles powered by other vehicle technologies that may prove to be more attractive than ours.

Our target market currently is serviced by manufacturers with existing customers and suppliers using proven and widely accepted fuel technologies. Additionally, our competitors are working on developing technologies that may be introduced in our target market. If any of these alternative technology vehicles can provide lower fuel costs, greater efficiencies, greater reliability or otherwise benefit from other factors resulting in an overall lower total cost of ownership, this may negatively affect the commercial success of our vehicles or make our vehicles uncompetitive or obsolete.

We currently have a limited customer base and expect that a significant portion of our future sales will be from a limited number of customers and the loss of any of these high volume customers could materially harm our business.

A significant portion of our projected future revenue, if any, is generated from a limited number of vehicle customers. Additionally, much of our business model is focused on building relationships with large customers. Currently we have no contracts with customers that include long-term commitments or minimum volumes that ensure future sales of vehicles. As such, a customer may take actions that affect us for reasons that we cannot anticipate or control, such as reasons related to the customer’s financial condition, changes in the customer’s business strategy or operations or as the result of the perceived performance or cost-effectiveness of our vehicles. The loss of or a reduction in sales or anticipated sales to our most significant customers could have an adverse effect on our business, prospects, financial condition and operating results.

Changes in the market for electric vehicles could cause our products to become obsolete or lose popularity.

The modern electric vehicle industry is in its infancy and has experienced substantial change in the last few years. To date, demand for and interest in electric vehicles has been slower than forecasted by industry experts. As a result, growth in the electric vehicle industry depends on many factors, including, but not limited to:

|

· continued development of product technology, especially batteries

|

|

|

· the environmental consciousness of customers

|

|

|

· the ability of electric vehicles to successfully compete with vehicles powered by internal combustion engines

|

|

|

· limitation of widespread electricity shortages; and

|

|

|

· whether future regulation and legislation requiring increased use of non-polluting vehicles is enacted

|

We cannot assume that growth in the electric vehicle industry will continue. Our business may suffer if the electric vehicle industry does not grow or grows more slowly than it has in recent years or if we are unable to maintain the pace of industry demands.

The unavailability, reduction, elimination or adverse application of government subsidies, incentives and regulations could have an adverse effect on our business, prospects, financial condition and operating results.

We believe that, currently, the availability of government subsidies and incentives is an important factor considered by our customers when purchasing our vehicles, and that our growth depends in part on the availability and amounts of these subsidies and incentives. Any reduction, elimination or discriminatory application of government subsidies and incentives because of budgetary challenges, policy changes, the reduced need for such subsidies and incentives due to the perceived success of electric vehicles or other reasons may result in the diminished price competitiveness of the alternative fuel vehicle industry.

We may be unable to keep up with changes in electric vehicle technology and, as a result, may suffer a decline in our competitive position.

Our current products are designed for use with, and are dependent upon, existing electric vehicle technology. As technologies change, we plan to upgrade or adapt our products in order to continue to provide products with the latest technology. However, our products may become obsolete or our research and development efforts may not be sufficient to adapt to changes in or to create the necessary technology. As a result, our potential inability to adapt and develop the necessary technology may harm our competitive position.

The failure of certain key suppliers to provide us with components could have a severe and negative impact upon our business.

We rely on a small group of suppliers to provide us with components for our products. If these suppliers become unwilling or unable to provide components, there are a limited number of alternative suppliers who could provide them. Changes in business conditions, wars, governmental changes, and other factors beyond our control or which we do not presently anticipate could affect our ability to receive components from our suppliers. Further, it could be difficult to find replacement components if our current suppliers fail to provide the parts needed for these products. A failure by our major suppliers to provide these components could severely restrict our ability to manufacture our products and prevent us from fulfilling customer orders in a timely fashion.

Product liability or other claims could have a material adverse effect on our business.

The risk of product liability claims, product recalls, and associated adverse publicity is inherent in the manufacturing, marketing, and sale of electrical vehicles. Although we have product liability insurance for our consumer and commercial products, that insurance may be inadequate to cover all potential product claims. We also carry liability insurance on our products. Any product recall or lawsuit seeking significant monetary damages either in excess of our coverage, or outside of our coverage, may have a material adverse effect on our business and financial condition. We may not be able to secure additional product liability insurance coverage on acceptable terms or at reasonable costs when needed. A successful product liability claim against us could require us to pay a substantial monetary award. Moreover, a product recall could generate substantial negative publicity about our products and business and inhibit or prevent commercialization of other future product candidates. We cannot provide assurance that such claims and/or recalls will not be made in the future.

We may have to devote substantial resources to implementing a retail product distribution network.

Dealers are often hesitant to provide their own financing to contribute to our product distribution network. As a result, we anticipate that we may have to provide financing or other consignment sale arrangements for dealers. A capital investment such as this presents many risks, foremost among them being that we may not realize a significant return on our investment if the network is not profitable. Our inability to collect receivables from dealers could cause us to suffer losses. Lastly, the amount of time that our management will need to devote to this project may divert them from performing other functions necessary to assure the success of our business.

Vehicle dealer and distribution laws could adversely affect our ability to sell our commercial electric vehicles.

Sales of our vehicles are subject to international, state and local vehicle dealer and distribution laws. To the extent such laws prevent us from selling our vehicle to customers located in a particular jurisdiction or require us to retain a local dealer or distributor or establish and maintain a physical presence in a jurisdiction in order to sell vehicles in that jurisdiction, our business, prospects, financial condition and operating results could be adversely affected.

While our products are subject to substantial regulation under federal, state, and local laws, we believe that our products are or will be materially in compliance with all applicable laws. However, to the extent the laws change, or if we introduce new products in the future, some or all of our products may not comply with applicable federal, state, or local laws. Further, certain federal, state, and local laws and industrial standards currently regulate electrical and electronics equipment. Although standards for electric vehicles are not yet generally available or accepted as industry standards, our products may become subject to federal, state, and local regulation in the future. Compliance with these regulations could be burdensome, time consuming, and expensive.

Our products are subject to environmental and safety compliance with various federal and state regulations, including regulations promulgated by the EPA, NHTSA, and various state boards, and compliance certification is required for each new model year. The cost of these compliance activities and the delays and risks associated with obtaining approval can be substantial. The risks, delays, and expenses incurred in connection with such compliance could be substantial.

Our success may be dependent on protecting our intellectual property rights.

We rely on trade secret protections to protect our proprietary technology. Our success will, in part, depend on our ability to obtain trademarks and patents. We are working on obtaining patents and trademarks registered with the United States Patent and Trademark Office but have not finalized any as of this date. Although we have entered into confidentiality agreements with our employees and consultants, we cannot be certain that others will not gain access to these trade secrets. Others may independently develop substantially equivalent proprietary information and techniques or otherwise gain access to our trade secrets.

We may be exposed to liability for infringing upon the intellectual property rights of other companies.

Our success will, in part, depend on our ability to operate without infringing on the proprietary rights of others. Although we have conducted searches and are not aware of any patents and trademarks which our products or their use might infringe, we cannot be certain that infringement has not or will not occur. We could incur substantial costs, in addition to the great amount of time lost, in defending any patent or trademark infringement suits or in asserting any patent or trademark rights, in a suit with another party.

Our electric vehicles make use of lithium-ion battery cells, which, if not appropriately managed and controlled, on rare occasions have been observed to catch fire or vent smoke and flames. If such events occur in our electric vehicles, we could face liability for damage or injury, adverse publicity and a potential safety recall, any of which could adversely affect our business, prospects, financial condition and operating results.

The battery packs in our electric vehicles use lithium-ion cells, which have been used for years in laptop computers and cell phones. On rare occasions, if not appropriately managed and controlled, lithium-ion cells can rapidly release the energy they contain by venting smoke and flames in a manner that can ignite nearby materials.

Our facilities could be damaged or adversely affected as a result of disasters or other unpredictable events. Any prolonged disruption in the operations of our facility would adversely affect our business, prospects, financial condition and operating results.

We engineer and assemble our electric vehicles in a facility in Loveland, Ohio. Any prolonged disruption in the operations of our facility, whether due to technical, information systems, communication networks, accidents, weather conditions or other natural disaster, or otherwise, whether short or long-term, would adversely affect our business, prospects, financial condition and operating results.

We have not paid dividends in the past and do not expect to pay dividends in the future. Any return on investment may be limited to the value of our common stock.

We have never paid cash dividends on our common stock and do not anticipate paying cash dividends in the foreseeable future. The payment of dividends on our common stock will depend on earnings, financial condition and other business and economic factors affecting the company at such time as the board of directors may consider relevant. If we do not pay dividends, our common stock may be less valuable because a return on investment will only occur due to stock price appreciation.

Our stock price and trading volume may be volatile, which could result in substantial losses for our stockholders.

The equity trading markets may experience periods of volatility, which could result in highly variable and unpredictable pricing of equity securities. The market price of our common stock could change in ways that may or may not be related to our business, our industry or our operating performance and financial condition. In addition, the trading volume in our common stock may fluctuate and cause significant price variations to occur. We have experienced significant volatility in the price of our stock. We cannot assure that the market price of our common stock will not fluctuate or decline significantly in the future. In addition, the stock markets in general can experience considerable price and volume fluctuations.

We have not voluntary implemented various corporate governance measures, in the absence of which, shareholders may have more limited protections against interested director transactions, conflict of interest and similar matters.

Recent Federal legislation, including the Sarbanes-Oxley Act of 2002, has resulted in the adoption of various corporate governance measures designed to promote the integrity of the corporate management and the securities markets. Some of these measures have been adopted in response to legal requirements. Others have been adopted by companies in response to the requirements of national securities exchanges, such as the NYSE or the NASDAQ, on which their securities are listed. Prospective investors should bear in mind our current lack of Sarbanes Oxley measures in formulating their investment decisions.

We may be exposed to potential risks relating to our internal controls over financial reporting and our ability to have those controls attested to by our independent auditors.

As directed by Section 404 of the Sarbanes-Oxley Act of 2002 ("SOX 404"), the Securities and Exchange Commission adopted rules requiring smaller reporting companies, such as our company, to include a report of management on the company's internal controls over financial reporting in their annual reports for fiscal years ending on or after December 15, 2007. We were required to include the management report in annual reports starting with the year ending December 31, 2009. Previous SEC rules required a non-accelerated filer to include an attestation report in its annual report for years ending on or after June 15, 2010. Section 989G of the Dodd-Frank Act added SOX Section 404(c) to exempt from the attestation requirement smaller issuers that are neither accelerated filers nor large accelerated filers under Rule 12b-2. Under Rule 12b-2, subject to periodic and annual reporting criteria, an “accelerated filer” is an issuer with market value of $75 million, but less than $700 million; a “large accelerated filer” is an issuer with market value of $700 million or greater. As a result, the exemption effectively applies to companies with less than $75 million in market capitalization. Item 9a of this filing, Controls and Procedures, indicates the company’s controls and procedures were not effective.

The trading of our common stock is limited under the SEC’s penny stock regulations, which will adversely affect the liquidity of our common stock.

The trading price of our common stock is currently less than $5.00 per share and, as a result, our common stock is considered a "penny stock”, and trading in our common stock would be subject to the requirements of Rule 15g-9 under the Exchange Act. Under this rule, broker/dealers who recommend low-priced securities to persons other than established customers and accredited investors must satisfy special sales practice requirements. Generally, the broker/dealer must make an individualized written suitability determination for the purchaser and receive the purchaser's written consent prior to the transaction.

SEC regulations also require additional disclosure in connection with any trades involving a "penny stock," including the delivery, prior to any penny stock transaction, of a disclosure schedule explaining the penny stock market and its associated risks. These requirements severely limit the liquidity of securities in the secondary market because few broker or dealers are likely to undertake these compliance activities. In addition to the applicability of the penny stock rules, other risks associated with trading in penny stocks could also be price fluctuations and the lack of a liquid market. An active and liquid market in our common stock may never develop due to these factors.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

Our principal offices are located at 100 Commerce Drive, Loveland, Ohio 45247, which include 7,500 square feet in office space and 22,500 square feet in manufacturing/development space. We pay $12,231 per month in rent and our current lease expires in September 2018. At December 31, 2013 approximately $17,133.46 is included in accounts payable for amounts due to the lessor. On March 13, 2013 the Company acquired the operating assets of Workhorse Custom Chassis, LLC, an unrelated company located in Union City, Indiana. The following summarizes the consideration paid, and the components of the purchase price and the related allocation of assets acquired and liabilities assumed:

|

Cash at closing

|

2,750,000 | |||

|

Secured debenture

|

2,250,000 | |||

| 5,000,000 | ||||

|

Assets acquired

|

||||

|

Inventory

|

400,000 | |||

|

Equipment

|

500,000 | |||

|

Land

|

300,000 | |||

|

Buildings

|

3,800,000 | |||

| 5,000,000 | ||||

ITEM 3. LEGAL PROCEEDINGS

We are currently not a party to any legal or administrative proceedings and are not aware of any pending or threatened legal or administrative proceedings against us in all material aspects. We may from time to time become a party to various legal or administrative proceedings arising in the ordinary course of our business.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our common stock was quoted on the OTCBB and OTCQB under the symbol "TTSO" from July 14, 2009 through May 24, 2010 and then under the symbol “AMPD” from May 24, 2010 to present. The following table sets forth the range of high and low prices per share of our common stock for each period indicated.

|

Quarter Ended

|

March 31

|

June 30

|

September 30

|

December 31

|

||||||||||||||||||||||||||||

|

High

|

Low

|

High

|

Low

|

High

|

Low

|

High

|

Low

|

|||||||||||||||||||||||||

|

2012

|

$ | 0.55 | $ | 0.20 | $ | 0.29 | $ | 0.11 | $ | 0.25 | $ | 0.10 | $ | 0.25 | $ | 0.08 | ||||||||||||||||

|

2013

|

0.37 | 0.12 | 0.53 | 0.23 | 0.51 | 0.23 | 0.30 | 0.10 | ||||||||||||||||||||||||

Holders of our Common Stock

As of April 10, 2014, there were approximately 79 stockholders of record of our common stock. This number does not include shares held by brokerage clearing houses, depositories or others in unregistered form. The stock transfer agent for our securities is Empire Stock Transfer, Inc., 1859 Whitney Mesa Drive, Henderson, Nevada 89014.

Dividends

The Company has never declared or paid any cash dividends on its common stock. The Company currently intends to retain future earnings, if any, to finance the expansion of its business. As a result, the Company does not anticipate paying any cash dividends in the foreseeable future.

Securities Authorized for Issuance Under Equity Compensation Plans

The following table sets forth the aggregate information of our equity compensation plans in effect as of December 31, 2013:

|

Plan

|

Number of securities to be issued upon exercise of outstanding options and rights

|

Weighted-average exercise price of outstanding options and rights

|

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in first column)

|

|||||||||

|

Equity compensation plans approved by security holders – 2010 Stock Incentive Plan

|

1,582,000 | $ | 0.42 | 388,250 | ||||||||

|

Equity compensation plans approved by security holders – 2011 Incentive Stock Plan

|

225,000 | $ | 0.70 | 775,000 | ||||||||

|

Equity compensation plans or arrangements not approved by security holders - 2012 Incentive Stock Plan

|

21,753,565 | $ | 0.77 | 1,441,500 | ||||||||

|

Equity compensation plans or arrangements not approved by security holders - 2013 Incentive Stock Plan

|

5,000,000 | $ | 0.28 | 2,500,000 | ||||||||

|

Total

|

23,560,565 | $ | 0.75 | 5,104,750 | ||||||||

Penny Stock Rules

The Securities and Exchange Commission has adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. Penny stocks are generally equity securities with a price of less than $5.00 (other than securities registered on certain national securities exchanges or quoted on the NASDAQ system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or system).

Our shares constitute penny stock under the Securities and Exchange Act. The shares will remain penny stocks for the foreseeable future. The classification of penny stock makes it more difficult for a broker-dealer to sell the stock into a secondary market, which makes it more difficult for a stockholder to liquidate his or her shares. Any broker-dealer engaged by the purchaser for the purpose of selling his or her shares in the Company will be subject to Rules 15g-1 through 15g-10 of the Securities and Exchange Act. Rather than creating a need to comply with those rules, some broker-dealers will refuse to attempt to sell penny stock.

The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from those rules, to deliver a standardized risk disclosure document, which:

|

· contains a description of the nature and level of risk in the market for penny stock in both public offerings and secondary trading

|

||

|

· contains a description of the broker's or dealer's duties to the customer and of the rights and remedies available to the customer with respect to a violation of such duties or other requirements of the Securities Act of 1934, as amended

|

||

|

· contains a brief, clear, narrative description of a dealer market, including "bid" and "ask" price for the penny stock and the significance of the spread between the bid and ask price

|

||

|

· contains a toll-free telephone number for inquiries on disciplinary actions

|

||

|

· defines significant terms in the disclosure document or in the conduct of trading penny stocks

|

||

|

· contains such other information and is in such form (including language, type, size and format) as the Securities and Exchange Commission shall require by rule or regulation

|

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, to the customer:

|

· the bid and offer quotations for the penny stock

|

||

|

· the compensation of the broker-dealer and its salesperson in the transaction

|

||

|

· the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the market for such stock

|

||

|

· monthly account statements showing the market value of each penny stock held in the customer's account

|

In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from those rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written acknowledgment of the receipt of a risk disclosure statement, a written agreement to transactions involving penny stocks, and a signed and dated copy of a written suitability statement. These disclosure requirements will have the effect of reducing the trading activity in the secondary market for our stock because it will be subject to these penny stock rules. Therefore, stockholders may have difficulty selling their securities.

Unregistered Sales of Equity Securities

On December 28, 2009, we entered into and closed a Share Exchange Agreement with the AMP Shareholders pursuant to which we acquired 100% of the outstanding securities of AMP in exchange for 14,890,904 shares of our common stock.

On December 28, 2009, the Company entered a Conversion Agreement with Bowden Transportation Ltd. (“Bowden”) pursuant to which Bowden agreed to convert a loan in the amount of $20,000 provided to AMP on December 21, 2009 into 500 shares of Series A Preferred Stock (the “Series A Stock”).

On December 28, 2009, the Company entered a Conversion Agreement with Han Solutions II, LLC (“Han”) pursuant to which Han agreed to convert a loan in the amount of $315,000 provided to AMP from October 28, 2009 through December 21, 2009 into 7,875 shares of Series A Stock.

The Series A Stock is convertible, at any time at the option of the holder into common shares of the Company based on a conversion price of $4.70588 per share. The Series A Stock has a par value of $0.001 per share. The holders of the Series A Stock are not entitled to convert the Series A Stock and receive shares of common stock such that the number of shares of common stock held by them in the aggregate and their affiliates after such conversion or exercise does not exceed 4.99% of the then issued and outstanding shares of common stock. The Series A Stock has voting rights on an as converted basis. Holders of the Series A Stock are not entitled to receive dividends and do not hold any liquidation rights.

On December 28, 2009, the Company entered a Conversion Agreement with Ziu Zhang (“Zhang”) pursuant to which Zhang agreed to convert a loan in the amount of $50,000 provided to AMP on November 30, 2009 into 148,932 shares of common stock of the Company.

On December 28, 2009, the Company assumed a Services Agreement entered between AMP and Pharmacy Management Services pursuant to which the Company issued Pharmacy Management Strategies LLC a common stock purchase warrant to acquire 500,000 shares of common stock at $0.40 per share for a term of five years. Half of the shares of common stock issuable under this warrant vested immediately and the balance vested one year from the date of the agreement.

On January 15, 2010, the Company entered a Subscription Agreement with Han pursuant to which Han acquired 625 shares of Series A Stock in consideration of $25,000.

From January 7, 2010 to March 4, 2010, the Company entered into subscription agreements with various accredited investors pursuant to which the investors purchased 1,042,062 shares of the Company’s common stock for an aggregate purchase price of $340,275.

On March 4, 2010, the Company compensated John Carris Investments LLC, as placement agent (“JCI”), for assisting in the sale of common stock by paying a commission in the aggregate amount of $35,528 and issuing JCI a common stock purchase warrant to purchase 105,704 shares of the Company’s common stock at an exercise price of $0.336 per share.

On March 1, 2010, the Company issued a 6% promissory note in the principal amount of $100,000 to an accredited investor in consideration of $100,000. In addition to the note, the lender also received a common stock purchase warrant to acquire 125,006 shares of common stock at an exercise price of $0.40 per share exercisable for a period of three years. The note had an interest rate of 6% per annum and was repaid in the third quarter of 2010.

From March 15, 2010 through October 22, 2010, the Company sold an aggregate of 7,256,000 shares of common stock for an aggregate purchase price of $2,902,400 to accredited investors. The closings occurred on the following dates:

On March 15, 2010, the Company sold 625,000 shares of common stock for an aggregate consideration of $250,000.

On April 7, 2010, the Company sold 200,000 shares of common stock for an aggregate consideration of $80,000.

On April 12, 2010, the Company sold 62,500 shares of common stock for an aggregate consideration of $25,000.

On April 16, 2010, the Company sold 112,500 shares of common stock for an aggregate consideration of $45,000.

On April 23, 2010, the Company sold 250,000 shares of common stock for an aggregate consideration of $100,000.

On May 6, 2010, the Company sold 175,000 shares of common stock for an aggregate consideration of $70,000.

On May 20, 2010, the Company sold 75,000 shares of common stock for an aggregate consideration of $30,000.

On May 25, 2010, the Company sold 75,000 shares of common stock for an aggregate consideration of $30,000

On May 28, 2010, the Company sold 500,000 shares of common stock for an aggregate consideration of $200,000.

On June 30, 2010, the Company sold 36,000 shares of common stock for an aggregate consideration of $14,400.

On July 7, 2010, the Company sold 175,000 shares of common stock for an aggregate consideration of $70,000.

On July 15, 2010, the Company sold 62,500 shares of common stock for an aggregate consideration of $25,000.

On July 22, 2010, the Company sold 1,125,000 shares of common stock for an aggregate consideration of $450,000.

On August 12, 2010, the Company sold 1,250,000 shares of common stock for an aggregate consideration of $500,000.

On August 27, 2010, the Company sold 375,000 shares of common stock for an aggregate consideration of $150,000.

On September 16, 2010, the Company sold 375,000 shares of common stock for an aggregate consideration of $150,000.

On September 22, 2010, the Company sold 1,625,000 shares of common stock for an aggregate consideration of $650,000.

On October 22, 2010, the Company sold 157,500 shares of common stock for an aggregate consideration of $63,000.

From March 15, 2010 through October 22, 2010, the Company compensated JCI as placement agent for assisting in the sale of common stock by paying it commissions in the aggregate amount of $290,240 and issuing the placement agent a common stock purchase warrants to purchase 725,600 shares of the Company’s common stock at an exercise price of $.40 per share.

On May 28, 2010, the Company assumed a Services Agreement entered between AMP and Mark Valerio pursuant to which the Company issued Mark Valerio an option to purchase 250,000 shares of voting common stock for a term of three years with a per share exercise option price of $0.40. The option vested as follows: 100,000 shares as of the date of May 28, 2010 (effective date); 50,000 shares within six months of the effective date; 50,000 shares within 12 months of the effective date; 50,000 shares within 18 months of the effective date.

On May 28, 2010 the Company assumed a Consulting Agreement with Pharmacy Management Strategies, LLC (“Pharmacy”) whereby Pharmacy will provide certain business development related services to the Company. As compensation for providing the services, the Company issued Pharmacy a common stock purchase warrant to acquire 350,000 shares of common stock for a period of five years at an exercise price of $0.40 per share, which vests quarterly in equal installments over a period of two years at a rate of 43,750 shares of common stock per quarter.

On June 1, 2010, the Company amended an October, 20, 2009 Services Agreement entered between AMP and CSIR Group, LLC for investor relations services, pursuant to which the Company issued CSIR 240,000 stock purchase warrants with an exercise price of $0.40 per share for a period of five years beginning June 1, 2010. The warrants vest equally in quarterly installments of 30,000 each. CSIR will be paid a fee of $7,500 beginning March 1, 2010 payable on the first day of each month.

On April 28, 2010, the Company assumed a Consulting Agreement entered between AMP and Gavin Scotti, Sr. pursuant to which the Company issued Gavin Scotti, Sr. a common stock purchase warrant to purchase 350,000 shares of common stock for a term of five years with a per share exercise option price of $0.40. The warrant vests equally in quarterly installments of 43,750 shares per quarter over two years. Additional compensation shall be paid if Mr. Scotti, Sr. is instrumental in raising capital through government or private capital as follows: $500,000 for raising up to $10,000,000; $750,000 for raising between $10,000,000 and $35,000,000; $1,000,000 for raising over $35,000,000 in financing.

On May 12, 2010, a Stock Incentive Plan was approved by the Board of Directors.

On September 28, 2010, the Company assumed a Services Agreement entered between AMP and Ron Sobrero pursuant to which the Company issued Ron Sobrero an option to purchase 100,000 shares of common stock for a term of three years with a per share exercise price of $0.70. The option vests as follows: 40,000 shares as of the date of September 28, 2010 (effective date); 20,000 shares within six months of the effective date; 20,000 shares within 12 months of the effective date; 20,000 shares within 18 months of the effective date.

On October 11, 2010, the Company entered into a letter agreement with James E. Taylor, a director of the Company. The Company agreed to pay Mr. Taylor $40,000 per year and issue Mr. Taylor an option to acquire 325,000 shares of common stock for five years with an exercise price of $0.68 per share. The options vest at 75,000 upon Mr. Taylor executing his letter of appointment and 50,000 every six months thereafter.

On December 8, 2010, Mr. Taylor entered into an employment agreement with the Company pursuant to which he was appointed as the Chief Executive Officer and Vice-Chairman of the Company in consideration of an annual salary of $300,000. Additionally, Mr. Taylor will be eligible for annual bonuses with a target amount of 100% of his salary. The actual amount of any bonus may be more or less than such target and will be determined by the board of directors in its absolute discretion. Half of the bonus may be paid, in the Company’s discretion, in unregistered shares of common stock at a price per share equal to the weighted average closing price per share of the common stock over the twenty most recent trading days prior to such grant. In addition to the salary and any bonus, Mr. Taylor will be entitled to receive health and fringe benefits that are generally available to the Company’s management employees. As additional compensation, the Company granted Mr. Taylor options to acquire 1,200,000 shares of common stock at an exercise price of $0.72 per share for a period of ten years. The Company also provided Mr. Taylor with a common stock purchase warrant to acquire 600,000 shares of common stock exercisable at any time in the five years following the signing of the agreement at an exercise price of $2.00 per share.

On December 8, 2010, Stephen S. Burns entered into an employment agreement with the Company pursuant to which he was appointed as the President of the Company in consideration of an annual salary of $200,000, however, only 50% of the salary ($100,000) will be payable at this time. The remaining 50% of the salary will accrue and be deferred until the board of directors elects to increase the salary to include all or a portion of the deferred salary based on certain events. Additionally, Mr. Burns will be eligible for annual bonuses with a target amount of 100% of his salary. The actual amount of any bonus may be more or less than such target and will be determined by the Board in its absolute discretion. Half of the bonus may be paid, in the Company’s discretion, in unregistered shares of common stock at a price per share equal to the weighted average closing price per share of the common stock over the twenty most recent trading days prior to such grant. In addition to the salary and any bonus, Mr. Burns will be entitled to receive health and fringe benefits that are generally available to the Company’s management employees in accordance with the then existing terms and conditions of the Company’s policies. As additional compensation, the Company granted Mr. Burns options to acquire 300,000 shares of common stock at an exercise price of $0.72 per share for a period of ten years. The Company also provided Mr. Burns with a common stock purchase warrant to acquire 300,000 shares of Common Stock exercisable at any time in the five years following the signing of the agreement at an exercise price of $2.00 per share.

From December 3, 2010 through March 29, 2011, the Company sold an aggregate of 3,364,983 shares of common stock and common stock purchase warrants to acquire 1,682,492 shares of common stock of the Company for an aggregate purchase price of $2,018,990 to accredited investors. The warrants are exercisable for two years at an exercise price of $0.80. In November 2012, the warrants were modified to change the exercise period from two years to three years. The closings occurred on the following dates:

On December 3, 2010, the Company sold 586,667 shares of common stock and Warrants to acquire 293,334 shares of common stock for an aggregate consideration of $352,000.

On December 17, 2010, the Company sold 483,333 shares of common stock and Warrants to acquire 241,667 shares of common stock for an aggregate consideration of $290,000.

On December 31, 2010, the Company sold 500,000 shares of common stock and Warrants to acquire 250,000 shares of common stock for an aggregate consideration of $300,000.